Tech Things: Netflix is buying nostalgia. Disney is buying OpenAI. OpenAI is buying time.

This is where I pretend to be a financial analyst and speculate wildly about things happening in the world

Netflix buys Nostalgia

Does Netflix count as a tech company? Am I allowed to write about this under the banner of tech things? Maybe it’s more like finance things? Or maybe money stuff? Who knows, I’ll leave it to the philosophy majors.

You may have heard that Netflix recently put in a bid to acquire Warner Brother’s Studios, to the tune of $80b. Earlier this year, WB’s market cap was something like $20b. Netflix is nearly quadrupling that price, and, importantly, is doing so with a lot of debt. Because everything has to be part of the culture war, Paramount put in a competing hostile bid. Paramount is run by David Ellison, son of Larry Ellison. The latter is CEO of Oracle and, importantly, is very buddy buddy with Trump. Rumors are swirling that the Ellison’s are trying to use their Trump connections to kill Netflix’s deal. Let’s just say, I wouldn’t be surprised.

In any case, when the deal was announced, Netflix stock dipped quite a bit. The markets overall seem rather unhappy with the deal, arguing that the price tag is far too high to justify. For the most part I’m uninterested in going beat by beat on the details of an M&A process. Instead, I want to boldly make the case that the market is wrong on this one. Full disclosure, I’m also talking my book. I just bought a bunch of Netflix.

To understand why Netflix wants WB so bad, you need to zoom out and think about what drives subscriptions. I think most people would say that new, good content drives subscriptions. In my opinion, this is compelling but subtly wrong.

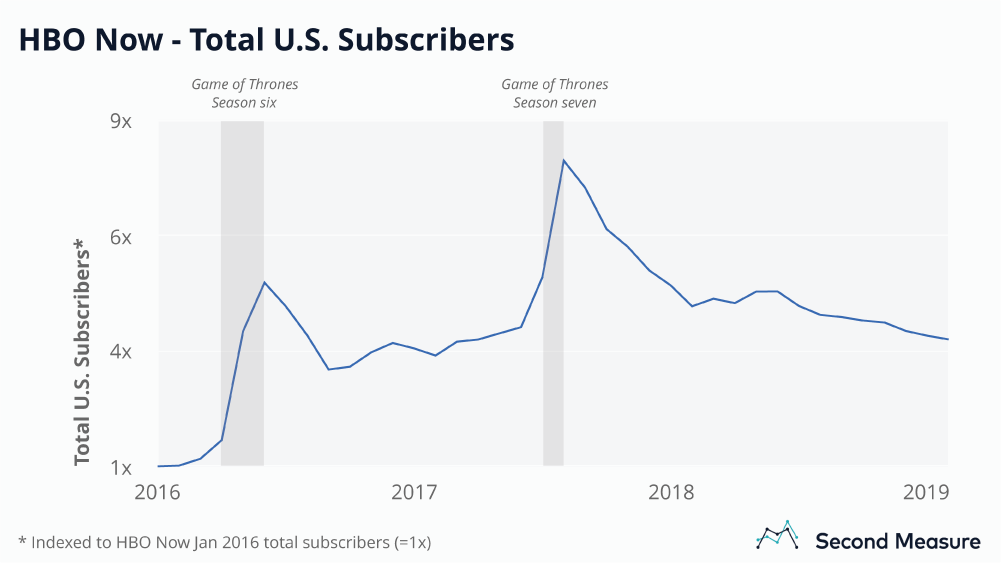

Here’s an example. Game of Thrones drove a TON of eyeballs to HBO. Following the above theory, Game of Thrones was good entertainment, and people like being entertained, so they would buy subscriptions to watch Game of Thrones. Makes sense on face. But Game of Thrones started in 2011. It didn’t really drive subscriptions until later seasons. Check out this graph:

Season 6 and season 7 of GoT resulted in nearly an order of magnitude subscriber growth from 2016.

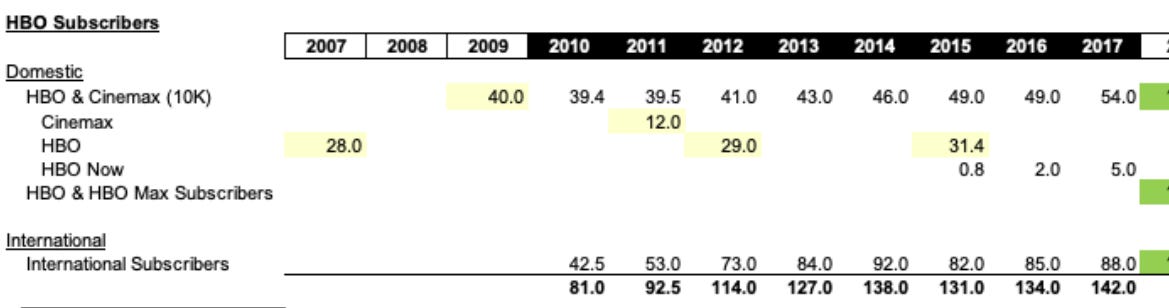

By comparison, here is the total subscriber counts from earlier years:

I don’t think GoT started bad and then got better. If anything, it was better in the earlier seasons! The show disconnected from the books at the end of season 5, and the further the show got from the books the worse it became. But it was the later seasons that generated the majority of the growth. As another contrast, Apple TV has fantastic content (Ted Lasso, Severance, Pluribus). So did AMC (Breaking Bad, Saul, The Walking Dead). But neither of them have really posted amazing subscriber growth — and I’m pretty sure both are actively hemorrhaging money.

“But Amol”, you might say. “This makes tons of sense. It takes time for the word to get out and for people to realize the content is good. You won’t see subscriber growth until you get buzz!” Well, yea. Subscriber growth is directly driven by fomo. More than good content, really more than anything else. GoT became a national phenomenon, and that drove the subscriber growth, not the other way around. In order to get subscriptions, the subscription services need to create cultural moments that center around their content. “O, you didn’t watch the latest season of Stranger Things x Squid Game? Guess you can’t participate in this conversation.” That drives subscriptions.

The problem is, creating cultural breakouts with original content isn’t easy. First, it’s really hard to consistently create good IP. Hopefully I do not have to prove this. And second, good content is only weakly correlated with breakout virality. Better Call Saul is objectively great TV, but it was never that influential. Meanwhile, everyone seems to be watching the latest season of Stranger Things, which is really just some of the worst shit I’ve ever seen.

But if all that’s true, why invest in good content at all? Much better to just recycle previous shows and movies that are known quantities and repackage them for new audiences. That’s partially why we’re seeing so many sequels and reboots and reruns. They are cheaper to get on the air and more likely to become popular.

Trying to generate hits with recycled content comes with its own issues though. If I have to download and pay for another service just to access a show or movie I’ve already seen, I’m not going to watch it. But if everyone follows that logic, no one will watch your recycled whatever! So you have a chicken and egg problem. You have all this content that people would happily pay for to avoid fomo. But you’re not going to be able to generate any fomo if it means customers have to lift a finger. You can only really create buzz if you can leverage some existing subscription base to make enough noise about your releases. In this, Netflix has a huge advantage.

There’s an old joke at Google that goes something like this:

Googler: My work on ads resulted in a $100m increase in revenue. I should be paid more!

[They removed a few log statements and made ads 0.001% more effective]

Any given hour of engineering time is simply far more economically productive at Google than it is virtually anywhere else.

The same is true at Netflix, but for IP. Netflix has a massive network. So the average piece of IP owned by Netflix is more valuable than if that same IP was owned by basically any other streaming service. And as a result, Netflix and Netflix alone has been able to consistently generate these cultural moments. Sometimes this is with new content — why did everyone get super into Queen’s Gambit? — but more often it’s with something old. The Office. Suits. Avatar: The Last Airbender. So many people signed up for Netflix for these old shows, because all the people who were nostalgic for those shows jumped on the chance to rewatch them when it was easy to do so. That cultural momentum then pulled new people into the network. Hell, the only reason I have a Netflix subscription is because I wanted to show my wife Avatar because everyone else was talking about rewatching the series! Anecdotally, targeted nostalgia seems to be the biggest generator of subscription volume.1 In a war for attention, nostalgia consistently drives conversation and conversion.2

With this lens, let’s take a look at WB’s IP.

Harry Potter. Lord of the Rings. DC. Looney Toons. Scooby Doo. Tom and Jerry. All of the Cartoon Network catalog like Adventure Time and KND and Dexter’s Lab. And of course, GoT. Nostalgia nostalgia nostalgia.

How many people have never seen the Harry Potter movies but have been surrounded, since birth, with their cultural impact? At least Gen Z was alive when the movies were still coming out, Gen Alpha has no context! They’ve just been hearing about sorting hats and talking snakes for years! The entire Harry Potter series is already available for streaming. You can watch it on YouTube premium and on Peacock and of course on HBO itself. But I feel pretty confident when I say that the day Harry Potter rereleases on Netflix is the day that everyone will organize the watch parties.

All of this underscores how ridiculous the Paramount counter bid is. $100b? A 5x market value multiple? Are you serious? Paramount buying WB would be a bit like a preindustrial society buying a bunch of shale. Yea, there may be oil there, but they can’t extract it. Only Netflix can. This is why I tend to be more sympathetic to the claims that Paramount is making a play for WB for primarily political reasons.

Bluntly, Netflix does not have real competition among streaming platforms. Disney should have been the main competition, thanks to their very deep bench of high quality high nostalgia IP. But Disney overplayed their hand by inundating the market to the point of fatigue. Maybe that fatigue could have been avoided with better content, but the criminal mismanagement of Disney’s studios, from LucasFilm to Marvel to Pixar, has led to a complete inability to generate hype and interest.

Nowhere is this more obvious than in the total cultural dominance of KPop Demon Hunters. Holy shit I cannot escape this movie. That music haunts my dreams, except actually it’s just the neighbor kids blasting Golden all night on repeat. You know what it all reminds me of? Frozen! KPop Demon Hunters is winning the exact demo (young girls and their parents) that Disney should have locked down. But if KDH launched on Disney+ instead of Netflix, it wouldn’t have gone anywhere. This, more than anything, is what would keep me up at night if I were a Disney exec. Obviously, Netflix can get more benefit from old IP than Disney can, but Disney can remain competitive just because it has a lot of the important IP already. However, if Netflix can also get people to at least try new IP, then they will be able to slowly erode Disney’s advantage.

I want to zoom out a bit to try and get at the trends that Netflix sees. Historically, we’ve thought of movies as its own media category. There was broad demand for something “movie shaped” — 2-3 hours of content centered around a single story played out in a theater. Hollywood has a lot of attachment and inertia around this idea. But the Internet has, bit by bit, chipped away at this vision. Increasingly, there is just content, and there is just consumer attention. All content has a certain production price, and all content has a certain attention payoff, and everyone is trying to maximize the amount of attention you get per dollar. This includes consumers! Part of the reason gaming is a growing industry is because the economics are great. I bought Silksong for the price of a movie ticket and got ~80 hours of entertainment out of it.3

In a world where everything is just content, Netflix’s real competition is, well, everyone else vying for consumer attention. That includes Tiktok and YouTube. But it also includes Valve (interactive media), Meta (social media), and arguably even the NYT (print media). I think this is why Netflix has been trying to get into gaming — something the WB purchase will also help accelerate.

The relative margins of short form video content are particularly scary for the Netflix business model. Making a viral Tiktok is cheap for Tiktok because the production costs are outsourced to the userbase. It is also cheap for Tiktok consumers, because the whole thing is mostly financed with ads. And even though Netflix is pretty good at generating fomo, Tiktok is even better. Still, nostalgia is, at least for now, a reasonable counter to the influencers influence. It’s not possible to recreate something like Lord of the Rings as a series of Tiktok dances. New content may all end up being driven into the ground by the production economics, but old content already exists. The production cost is, technically, 0. So Netflix wants WB, the home of nostalgia. If content quantity powers the Netflix growth engine, acquiring WB is like turning on a nuclear reactor.

The reason the market is skittish about this deal is because $80b is simply a lot of money. Netflix charges ~$20 per month per subscription. So even if you assume all of the 130 million existing HBO subscribers seamlessly transfer over and don’t have existing Netflix accounts, Netflix still would need to get and retain ~200 million additional signups for at least a year to break even. That’s a lot of people, most of whom will have to be outside of the US.4

But Netflix is playing the long game. I think with the right IP, the same fomo dynamics apply. WB is a bet that Netflix can leverage its existing dominance to drive excitement about long dead franchises for years to come, franchises that it can pick up for relatively cheap now. If they are right, they own the future of all content longer than a thirty second doom scroll.

Disney buys OpenAI

If I’m hungry, and I go into a McDonald’s and buy a burger, there’s a transaction that takes place. I pay $5 or so, and in exchange, I get a mediocre-but-delicious sandwich. This is called a “sale”. Everyone acknowledges that something was traded for something else, and these two things are roughly of equal value.

If I’m a VC, and I go to a startup and I buy some equity, there’s also a transaction that takes place. I pay $5m or so, and in exchange I get 2 million shares of a likely mediocre lottery ticket. This is called an “investment”, which is different from a sale. It sorta looks like a sale. And in fact technically it is a sale, at least to the folks at the IRS. But the connotation is different. When a VC invests in a startup, generally the sense is that the startup is the one that benefits. The VC is giving $5m for a bunch of IOUs that are, technically, worth basically nothing. Or at least, they are worth nothing right now. When I buy a burger, I’m getting $5 worth of burger at that moment. When a VC buys $5m worth of startup shares, they’re buying $200m of potential value for later.

Still. If you were a particularly annoying kind of person, you could argue that when I go to McDonald’s, I’m investing in McDonald’s in exchange for the burger. That would be a very strange use of terminology, but strictly it wouldn’t be a lie.

Anyway, this past week OpenAI announced that Disney was investing $1b in OpenAI. In exchange, OpenAI is getting the right to generate Disney characters. If you think of an investment as something broadly favorable to the person getting the investment, this set up makes no sense. Disney should be getting something for its investment! Why is OpenAI getting the money and the rights?

My crackpot, totally unsubstantiated theory: Disney didn’t actually transfer any money.

OpenAI primarily caters to consumers. Consumers want to do silly things like talk to Mickey Mouse and generate AI pictures of Mickey Mouse. Thanks in part to Disney’s very active legal department, this is illegal. Every time someone gets ChatGPT to create a mouse with red shorts and white gloves, a Disney lawyer gets their wings. As a result, OpenAI has strict guardrails to try and stop consumers from doing what they want. This is, obviously, a worse user experience, and isn’t going to stop a really motivated user anyway.

Maybe OpenAI got in touch with Disney to try and get some kind of licensing agreement. Or Disney reached out to OpenAI with a cease and desist and a threat of litigation. Disney probably said something like “licensing our content costs $1b. Pay up or we sue.” And Sam probably said something like “uhh well, we don’t have $1b. But how about we give you $1b worth of equity? Just one small favor: when we report this to the press, let’s just call this an investment.”

The reporting makes it seem like there was an “investment” of $1b in cash for $1b of OpenAI equity, and separately Disney was giving OpenAI license to the House of Mouse for free. The “and“ in the WSJ title above is doing a lot of work. But I think the content licensing was the investment. Disney gave $1b worth of licensing value in exchange for $1b of stock. Suddenly this starts to feel less like an investment and more like a standard sale, just denominated in a slightly weird way. But you can see why the framing helps OpenAI. “OpenAI gives up equity to avoid Disney lawsuit” sad, pathetic, likely to crash the entire world economy. “Disney invests in OpenAI” strong, majestic, successful, rocketship that definitely won’t crash the entire world economy

As an aside, it is a bit interesting that Disney would agree to this at all. Disney has literally gone after daycares that had Mickey drawn on the walls for copyright infringement. They care a lot about their brand, and have strong prohibitions for showing any of their characters in compromising situations. And now they turn around and let their IP loose on an AI video generator? It’s weird! Maybe Disney sees the writing on the wall — they can’t stop the AI wave, so they may as well get paid. In any case, I expect a lot of, uh, adult content related to Disney characters coming up soon.

OpenAI buys time

What does it mean when OpenAI announces that we have gone from GPT4 to GPT5?

Here’s how an engineer might answer:

A modern LLM is composed of a few distinct steps. There’s a pretraining step, where you shove all of the internet into the model. This defines the ‘knowledge-cutoff’ of the model — the information that is baked into the model weights. And there’s a set of posttraining steps, where you fine tune the model on things like ‘answering questions’ and ‘being helpful’. Naturally, every time you release a new model that is a fine-tuned version of some pretrained model, you increment the decimal. And naturally, every time you release an entirely new pretrained model, you increment the main version number. Naturally.

Here’s how a marketing team might answer:

Screw that nerd shit, the number goes up when we need to generate hype.

A few months ago, OpenAI released…something…called GPT5. It was a bit of a dud. I wrote about that here.

Then they released something called GPT5.1 about a month ago. And this was a bit better than GPT5, as one would expect from a version upgrade. And more recently, they just released GPT5.2.5 If you were an engineer, you may think that GPT5, 5.1, and 5.2 are all variants of the same pretrained model — that GPT5.1 and GPT5.2 are finetuned versions of GPT5 — because that’s how basically everyone has done it till now. But I think that’s wrong. The evidence is the cutoff dates.

GPT4o had a knowledge cutoff of June 2024. Both GPT5 and GPT5.1 have knowledge cutoff dates for just a few months later, September 2024. That means that at the time of release, GPT5 had not had a pretraining run for nearly a full year. If you’re going by the ‘engineering’ naming scheme, GPT5 and GPT5.1 really ought to be called GPT4.2 and GPT4.3. The latest GPT model, 5.2, is the first major OpenAI model to actually have a 2025 knowledge cutoff date! Which means, drumroll introducing the real GPT5!

I do wonder, though. What was going on in August that led OpenAI to announce GPT5 in early August?

O. Yea, that makes sense. It’s probably easier to close a big fundraising round when you can show investors ‘GPT-5’. It’s not like the investors will be able to tell the difference. The marketers get a salary for a reason.

Anecdotally, the overall feedback for GPT5.2 is significantly better than for 5.0. Which is reasonable, since a) this is the actual GPT5 model6 and b) the hype train has derailed for a bit so people aren’t benchmarking against unrealistic standards.

I would love to say ‘empirically’ here, but from the outside looking in, it is very difficult to disentangle Netflix subscriber growth from any given release or piece of content. I think they like it this way.

This is also why Netflix keeps investing in things like the One Piece or Cowboy Bebop live actions — they are reskins of nostalgic content, a way to piggy back on old ip to try and create momentum.

Assuming the average movie is about 2 hours long, I got 40x the RoI on Silksong than what I would’ve gotten if I just actually went to the movies.

Netflix has 90m subscribers in the States, which is a bit more than one in every 4 people. Virtually anyone who wants access to Netflix stateside can get it.

Possibly in response to Gemini 3’s stellar release.

I’m an engineer, not a marketer. Sue me.

Love the take, great writing

Great writing! You could say that short form media (mainly TikTok in this case) can won’t take away from Netflix’s nostalgic cultural moments but actually help bolster it. After watching let’s say the Harry Potter movies after it’s re-released on Netflix, people will flock to TikTok to talk about it which would make the cultural moments even stronger. Also, because you’re able to reach hundreds of millions of people on TikTok, there would be an even stronger sense of fomo.